In my earlier report, I stressed that Spain's Q1 surge was as much a statistical artifact as anything else since:

a) Nominal GDP growth was virtually stagnant, and the application of the (negative) GDP price deflator (see explanation in earlier report below) explained most of the annual growth.

b) Spain's strong export drive has stalled, with exports being little changed in March 2014 from September 2013.

c) There was a major input from government spending. An important part of the explanation for the momentum behind Spain's recovery has been the relaxation of austerity, and the strong injection of government funded liquidity into the economy.

All these three trends are confirmed by the latest data, albeit, as I say, with significant nuances.

GDP deflator: Inter-annual real GDP growth was revised to 0.5% from the 0.6% in the INE flash estimate. More importantly we learnt today that nominal GDP fell 0.1% over the year, confirming the impression that despite the recovery people had less money in their pockets (this is what deflation means).

Export recovery: exports fell by less than originally estimated (by 0.4% quarter on quarter rather than by 0.6%) but the big change came in imports which moved from an estimated fall of 1.2% (q-o-q) to a rise of 1.5%. The net trade contribution to the final GDP number thus swang from being 0.2% positive to 0.2% negative. However the impression that this is no longer an export lead recovery was confirmed, as was the fear that as government-stimulus fed domestic demand imports would once more surge. This seems to confirm the idea that the economy is not as internationally competitive as the official sector claim it is.

Government spending: the big shocker in the latest report is the role played by government spending in arriving at the final number. The Bank of Spain only mentioned there had been an increase, giving no estimate for its magnitude. Today we learn that government spending was up 4.4% on a quarterly basis, following a 3.9% decline in the last quarter.This confirms the impression that there was a significant ending-the-budget-year-early effect (see original report below), as spending was transferred from Q4 2013 to Q1 2014. It also confirms the impression obtained from the Q1 labour force survey where we learnt that while private sector employment contracted during the first three months of the year, public sector employment rose by 11,100. Naturally, if the government is to comply with this years reduced deficit target this momentum cannot be maintained, suggesting we will now see some weakening in the headline GDP number.

In fact in their latest report on the Spanish economy (published May 28) the Bank of Spain confirm this impression, saying that "Los indicadores coyunturales más recientes apuntan, en general, a una prolongación de la fase de recuperación de la actividad, si bien se aprecia distinta intensidad según se trate de información procedente de indicadores cualitativos o cuantitativos". Roughly translated this means that the recoverey phase has continued into the second quarter although the intensity may have reduced according to which indicator you look at (hard and soft). They cite the EU household confidence indicator, which continued to improve in April but less than in the previous three months. Also sales (both of goods and services) by large companies moderated their annual growth rates in March compared with earlier months. To me it looks like Q2 quarterly growth will be weaker than Q1. possibly in the order of 0.2%.

Construction activity is an interesting area. The INE Q1 report suggests a quarterly decline in construction activity of 2.6%, yet data supplied by the INE to Eurostat show a 9% rise during the quarter, an improvement that is consistent with other information available. Spain has something like 400,000 unfinished houses and bad bank Sareb and investment funds who have purchased distressed property loans appear to be finishing some of these housing units off in readiness to let.

All in all the argument I am pursuing here is not that Spain's economy isn't recovering - it is - but that the recovery is much weaker and much less well balanced than many think it is. Momentum going forward looks weaker than people expect, employment growth is tepid (except in the public sector), and the fall in unemployment is as much a product of people leaving the country or retiring as of anything else. Spain is already in deflation, house purchases continue to be postponed awaiting a further fall in prices, and the hard won rebalancing of the economy towards external trade is steadily being undermined.

Perhaps just one data point sums this whole problem up. According to seasonally adjusted data, nominal GDP rose by 1.432 billion euros during the quarter, while nominal government spending rose by 2.494 billion euros (or almost double). Not a very impressive bang for the buck. Go figure.

Spain: The Land Where Incipient Deflation Becomes Good News For Headline GDP - 25 April original review

.

According to the bank of Spain, the Spanish economy continued to push forward with its recent expansion in the first quarter, and it do so at an accelerated rate, growing by 0.4% over the previous three months. This is certainly good news for everyone in Spain, and there is no doubt that this is the strongest expansion in economic activity (see PMI chart below) since the crisis started. The economy also grew by 0.5% over a year earlier, the first time it has done this in nine quarters.

Nonethless many of the old doubts about the durability and sustainability of the Spanish expansion remain. The labour market is still a huge problem, the housing market is gridlocked, credit is scarce and expensive, and the population is shrinking at nearly 1% a year as discouraged workers (both nationals and former migrants) pack their bags and leave. In addition, concerns are mounting that the current government, with low ratings in the polls and elections coming next year, has lost the appetite for reform. Here I will focus on three issues that strike me in connection with the latest GDP numbers: the stagnation in the export boom, the difficulties being encountered in reducing the deficit and the ongoing deflation issue. The big question still remains: is this a balanced recovery, an export lead one, or simply a government financed one?

Composition of Growth

Here to help think about all this is the Bank of Spain breakdown of recent economic growth.

GDP is a composite, derived by aggregating a number of components. Principal among these are private consumption and investment, public consumption and investment and net trade. If we look at the composition of growth in Spain in the first three months of this year we find that private consumption grew, but less rapidly (0.3 vs 0.5) than in the preceding three months, government consumption and investment grew (vs contraction at the end of last year) but we don't know by how much because, unfortunately, the BoS don't tell us. Net trade was positive - despite the fact that both exports and imports were down (on a seasonally adjusted basis, by 0.6% and 1.2% respectively). Since imports were down by more than exports, net trade was positive and contributed an estimated 0.2 percentage points (or half) to growth. If imports had fallen by less, by say only 0.6%, then Spanish GDP would only have grown by half (0.2%), such are the quirks of GDP calculations. But it is surely not unequivocally good news if you have had to rely on a slump in imports to get that highest-growth-in-recent-years number.

Lastly Spain is officially in deflation, both of the falling expectations and purchases postponement kind - see this post yesterday - and this is recognised by the presence of a negative GDP deflator, which estimates a fall of 0.4% in GDP price inputs when compared with a year earlier. More on this later.

What is going on with exports?

Spanish exports have been an important part of the country's recovery story, no doubt about that. Services exports (mainly tourism) have been up consistently. But if Spain is to become "the new Germany", and this is what will be needed (current account surplus and all) if the country is to return to stable growth, goods exports need to grow and keep growing at a steady rate, and this is where the evidence we have to hand is a little less than convincing.

So in fact while the export story does continue on a modified basis, with growth in the Euro Area picking up some of the slack left by the demise of the EM customer base, it is a long way from being as vibrant as it was. This tendency is clearly revealed in the latest press release from the Economy Ministry covering exports (for February). While in the whole of 2013 export to the Euro Area were only up 0.1%, in January and February of 2014 they were up by 5.5% from a year earlier. Meanwhile exports to non EU destinations were only up by 0.4% over last year even though exports to the US, China and Japan all increased by significant percentages.

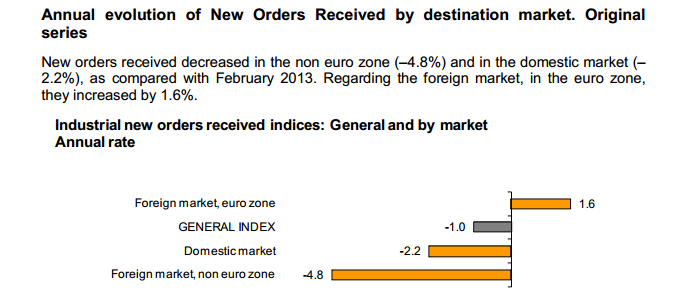

Not only are goods exports when compared with six months earlier rather stationary at the moment, the order books suggest the situation won't be improving radically in the coming months as the following chart from the national statistics office illustrates.

Overall new orders were down year on year by 1% in February, with orders from the domestic market - which were down by 2.2% - dragging the aggregate with it. Export orders were positive, but the composition changed, with demand from the Euro Area up 1.6%, while orders from outside the EA were down by 4.8%.

This division between improving export orders and weakening domestic ones is an ongoing story, as the following chart, again from the INE, illustrates. The interesting line is the seasonally adjusted one, and it shows that only in two months in the last two years - December 2013 and August 2012 - have industrial orders been above the level of a year earlier.

This phenomenon is due to the enduring weakness of domestic demand, and even with the recovery the pattern doesn't seem to have been radically altered. Industrial output is up, but only very very marginally, hardly noticeably even in the great scheme of things.

In the meantime, the fact that domestic demand is rising has been having a negative impact on the evolution of the goods trade balance, which after hitting a historic surplus high last March has been in deficit territory almost ever since.

Indeed if we look at the trend, after steadily reducing the deficit has once more stabilized well in negative territory. So while Spain's export sector has made considerable progress - more than most, but then the country's problems are greater than most - there is still a long road left to travel. Most importantly a net trade impact based on a sharp fall in imports is not what we should be seeing at a point where the recovery is gathering traction. It does not suggest a broadening out into steadily improving domestic consumer demand, but quite the contrary.

Deficit Difficulties

Spain, as is well known, was given extra time by the EU Commission - 2 additional years - to bring its fiscal deficit down below the 3% of GDP mark. In fact the country has made enormous efforts to reduce the deficit, but the results of such efforts have often been far less than had been hoped for. After hitting a peak of 11.2% of GDP in 2009, the deficit figure has meandered from 9.7% in 2010 to 9.6% in 2011 to 10.8% in 2012, to finally reach 6.6% in 2013. Not surprisingly this deficit record has produced a rather astonishing surge in the government debt level, from 36% of GDP at the onset of the crisis in 2007 to the current level of nearly 100%.

But even this 2013 6.6% number is not everything it seems to be, since the government was forced to draw down some 2% of GDP extra from the pension reserve fund (intended to help get the country through the difficult demographic moment that arrives at the end of the decade) and a further 1% of GDP from the Suppliers Fund (which is to pay suppliers previously unpaid bills). Neither of these liquidity injections affects the EDP deficit, but both certainly help the government square the difference between spending and income. Even so, in order to maintain the 6.6% number (actually it should have been 6.5%) the government was forced to draw the budget year to a close on November 25.

As reported in March in the Bloomberg article - Spanish Government Ended 2013 in November to Reduce Deficit - Spain brought forward the deadline for approving spending in the annual budget for the second straight year in 2013 following a 2012 decision to end the year on December 3. Previously the cut-off date had been the last working day of the year. Hence the enigmatic statement from the Bank of Spain that both government consumption and investment grew in Q1 following "their marked decline in the closing months of 2013". The marked decline was partly due to the cut-off date, so for deficit compliance reasons some of the spending was transferred to Q1 2014, giving a small boost to the headline GDP number.

In fact, the EDP accounting measure is becoming an increasingly blunt instrument for measuring the extent of Spain government spending and the dynamic of its debt obligations. According to Bank of Spain data there were something like 1.35 trillion euros of Spain government debt obligations in circulation at the close of 2013, as compared with the 961 billion euros worth which count as debt under EDP rules. I dealt with this issue at some length a couple of years back, but leaving aside the details - groso modo - it is clear that there is much more Spanish debt out there than many are assuming. Even more surprising is the fact that total debt obligations rose by some 14.5% during 2013, and that 56% of this increase came under headings which don't count towards the EDP measure.

The Role of the GDP Deflator

Finally we come to what may well be the most important doubt that enters my head when I look at that Bank of Spain table I reproduce above: the role played by the magnitude of the GDP deflator in arriving at the headline GDP number. The GDP deflator is the measure that is used to convert nominal (current prices) GDP into real (comparing apples with apples and not with pears) GDP, since it is an attempt to remove the impact of price movements (inflation or deflation) from the final benchmark GDP reading. Let's take an example. If nominal GDP grows 5% and inflation is 3% then real GDP has grown by 2%. If inflation is then re-estimated at 2% then real GDP growth turns out to have been 3%, and so on. Compensating for deflation is when things start to get more complicated, and doing so when nominal GDP is either stationary or negative is when the world gets really wonky.

Lets take the case where nominal GDP grows by 2%, and deflation is 1% - then real GDP grows by no less than 3% (you have to add the deflation number, not subtract the inflation one, if in difficulty ask the Japanese for help, they have been doing this for years). Now lets imagine a case where quarterly nominal GDP growth is zero, but the GDP deflator is estimated at minus 0.4% (aha, now you see where I am going). Then in this case real GDP grows on the quarter by 0.4% (precisely the current Spanish result). Supposing that later you revise this estimate to minus 0.2%, then GDP growth is halved at a stroke, since it also becomes 0.2%.

I am not the first person in the world to to think about this issue, and especially not in connection with Spanish GDP data. Back in August last year the UK economist Shaun Richards wrote a blog post - What is happening with the national accounts and GDP of Spain? - which dealt with a number of similar issues. Shaun examines the impact of a series of data revisions carried out at the end of Q2 2013 and draws some thought provoking conclusions.

In particular he examines the impact of a number of statistics office revisions to the GDP deflator estimates. As he tells us,

"we get a new view on Spain by observing that it (the estimated GDP deflator) has been effectively zero since the end of 2008. I am slightly exaggerating as in fact it adds up to 0.17% but I hope that you get the point. The revisions here have been large as the number was previously 1.58%! Now consider GDP numbers which are sometimes poured over for 0.1% and we see one more time that such behaviour is bizarre as they are by no means that accurate. Indeed 2011 seems to be a troubled year for Spain’s accounts as implied deflator inflation was 0.96% and is now 0.02% which is much more like 1% than 0.1%."Certainly then the GDP deflator plays a very central role in final Spanish GDP outcomes, and the sensitivity of the early GDP estimates to errors in the deflator value is striking. As I am suggesting here the value attributed for Q1 2014 effectively accounts for 100% of the estimated GDP growth, and the probability of subsequent revision is, going by past experience, large. Indeed in the Spanish context could it be said to be the loop which finally squares any unfortunate circular gaps in the national accounts?

And when I said when nominal GDP is close to zero things get wonky, I meant it. According to data from the Spanish national statistics office, seasonally adjusted nominal quarterly GDP hasn't budged more than a decimal point from 255 billion euros since Q2 2013 (see chart below), and even then the decimal movement has been downwards. We don't have an estimate for the first quarter of this year yet, but if the 0.4% real growth and the minus 0.4% GDP deflator estimates are confirmed, then it should be just about where it was during Q4 2013.

I was surprised to find this, but then maybe I shouldn't have been since shopkeepers have been telling me for months that the takings in their tills hadn't improved. Now we know why. There has been an improvement in output VOLUME and COMPOSITION, since prices have been falling and the economy has reorientated somewhat, but not in overall turnover. Looking at these numbers one of two things are true. Either Spain has been sliding steadily into deflation over the last year, or there has been no recovery. There would seem to be no available third reading. The most probable interpretation of the data we have to date would be the former, that Spain is sinking steadily into deflation. I assume the statisticians at the economy ministry understand GDP calculations sufficiently to get this. In which case the constant denials, and references to early Easter "one offs" etc would seem to be totally irresponsible.

So, the ability of the Bank of Spain to offer an early estimate (normally confirmed by the INE first estimate) of GDP growth - based on the variables included in the economy ministry's synthetic indicator - comes at a price: you need to wait 12 or 18 months to get a much more precise measure of what is going on. As Shaun says:

One of the issues with Gross Domestic Product numbers is that they are revised over time sometimes significantly. This does not fit well with the short attention span of modern media and so leads to an obvious temptation to publish relatively optimistic figures and then revise them later once the hue and cry of the pack has died down.

Conclusions

As I state at the outset, I have no doubt whatsoever that Spain's economy is undergoing a modest recovery. Even economy minister Luis de Guindos calls it weak, fragile and uneven. Serious doubts exist about the extent to which we are going to see anything resembling a "classic recovery" in Spain, a recovery where solid export growth eventually broadens out into a wider improvement in domestic consumption and investment, even though this is what financial markets increasingly seem to be pricing in. Press headlines have trumpeted the country's new found growth, but when you dig under the surface and find that most of the latest growth is either accounted for by a sharp DROP IN IMPORTS, or by a CALENDAR ADJUSTMENT IN GOVERNMENT ACCOUNTING, or by the ESTIMATED ARRIVAL OF DEFLATION then the conclusions you draw are hardly reassuring ones.

If in addition these highly-subject-to-later-revision initial estimates are used by the incumbent government to try to shore up its wobbly position, and also used as an justification for not carrying out deeper reform - especially in the labour market where unemployment remains over 25% - then beyond not being reassuring they start to become preoccupying.